Because Puerto Rico is a U.S. territory, not a state, its sales tax system is separate from other U.S. jurisdictions.

Sales and use tax in Puerto Rico is called Impuesto sobre Ventas y Uso (IVU). If you have nexus in Puerto Rico, you must collect IVU, file, and remit payment through the Sistema Unificado de Rentas Internas (SURI), which translates to the Unified Internal Revenue System.

The tax rate on most sales is 10.5% at the state level, and an additional 1% local tax for a combined 11.5% rate. The due date for filing and remitting payments is the 20th of each month.

Not all tax compliance software helps you fulfill requirements if you sell within Puerto Rico, so it’s important to account for their rules if you sell to customers there.

This guide goes over the steps to filing and remitting sales tax (IVU) using Puerto Rico's SURI platform.

[blog-post-inline-cta]

How to file sales tax (IVU) in Puerto Rico

Here’s the end-to-end process for filing sales tax (IVU) in Puerto Rico, including getting registered for the first time with SURI.

If you've already registered and just need to know how to file, you can skip to Step 3.

Step 1: Register as a merchant through SURI

Before you can collect sales tax anywhere, you must register with the state or, in this case, the territory. In Puerto Rico, you need a Certificado de Registro de Comerciante, or Merchant's Registration Certificate, to be legally authorized to collect.

Registering for the Certificate is free. It's actually required of all businesses 30 days before starting operations, including home-based and temporary companies.

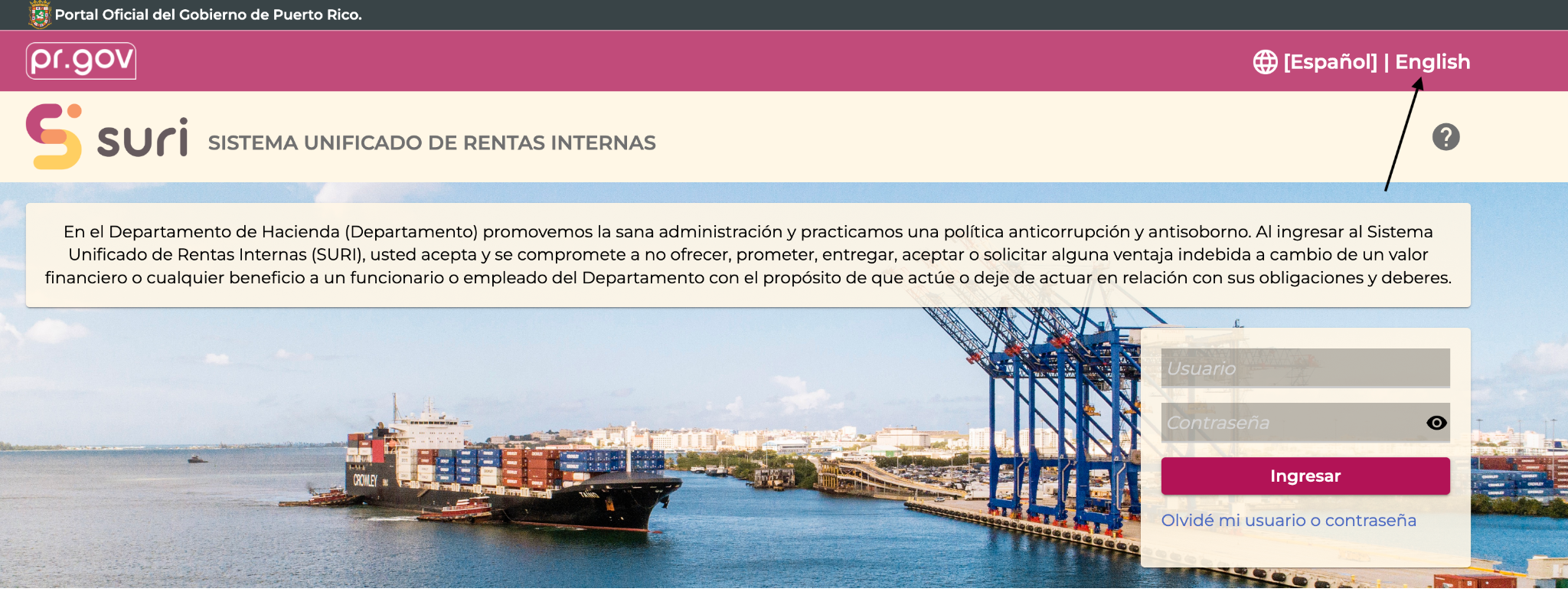

To obtain your certificate, visit suri.hacienda.pr.gov. If you don't already have a business account, you will need to complete the application inside SURI to register for one.

The default language on the website is Spanish, but you can change the language to English using the toggle in the upper right.

To complete your registration, you must provide:

- Your EIN

- Your business name and DBA (if applicable)

- Your business address

- The type of goods or services sold

- Your expected sales volume in Puerto Rico.

After you've created an account and logged in, navigate to the registration section and apply for the Certificate by completing Form AS 2914.1.

Important: Do not wait until after you start selling to register in Puerto Rico. The penalty for late registration could go as high as $10,000.

Step 2: Collect the right amount from customers

In Puerto Rico, the majority of physical goods and digital products, including SaaS, are taxable at the 11.5% rate. However, there are exemptions, including for unprepared groceries and prescription drugs. There is also a reduced rate in place for some B2B transactions.

You must charge customers tax at the correct rate, so check the table below or the territory's guide to exempt items to understand when you must charge tax.

You'll also need to keep detailed records of:

- Total gross sales

- Taxable sales

- Exempt sales

- IVU collected

You'll need all this information when you submit your returns.

Tip: If you sell through a "marketplace facilitator," the platform may collect IVU on your behalf. Marketplace facilitators are platforms like Amazon or Etsy that play an active role in the sales transaction. For example, Shopify isn't a marketplace facilitator, but Shopify's "Shop" app is. Verify with the sites you sell on whether the site is a marketplace facilitator and, if so, whether it handles your tax obligations in Puerto Rico.

[blog-post-inline-cta]

Step 3: Log in to SURI and file your return

After collecting the correct tax, you must file your tax return by logging into SURI. Typically, returns must be filed monthly and are due by the 20th of the month following a taxable sale.

This means that a return for April's sales must be filed by May 20th. If the 20th falls on a weekend or holiday, the deadline shifts to the next business day.

To file your return, log in to suri.hacienda.pr.gov using your credentials.

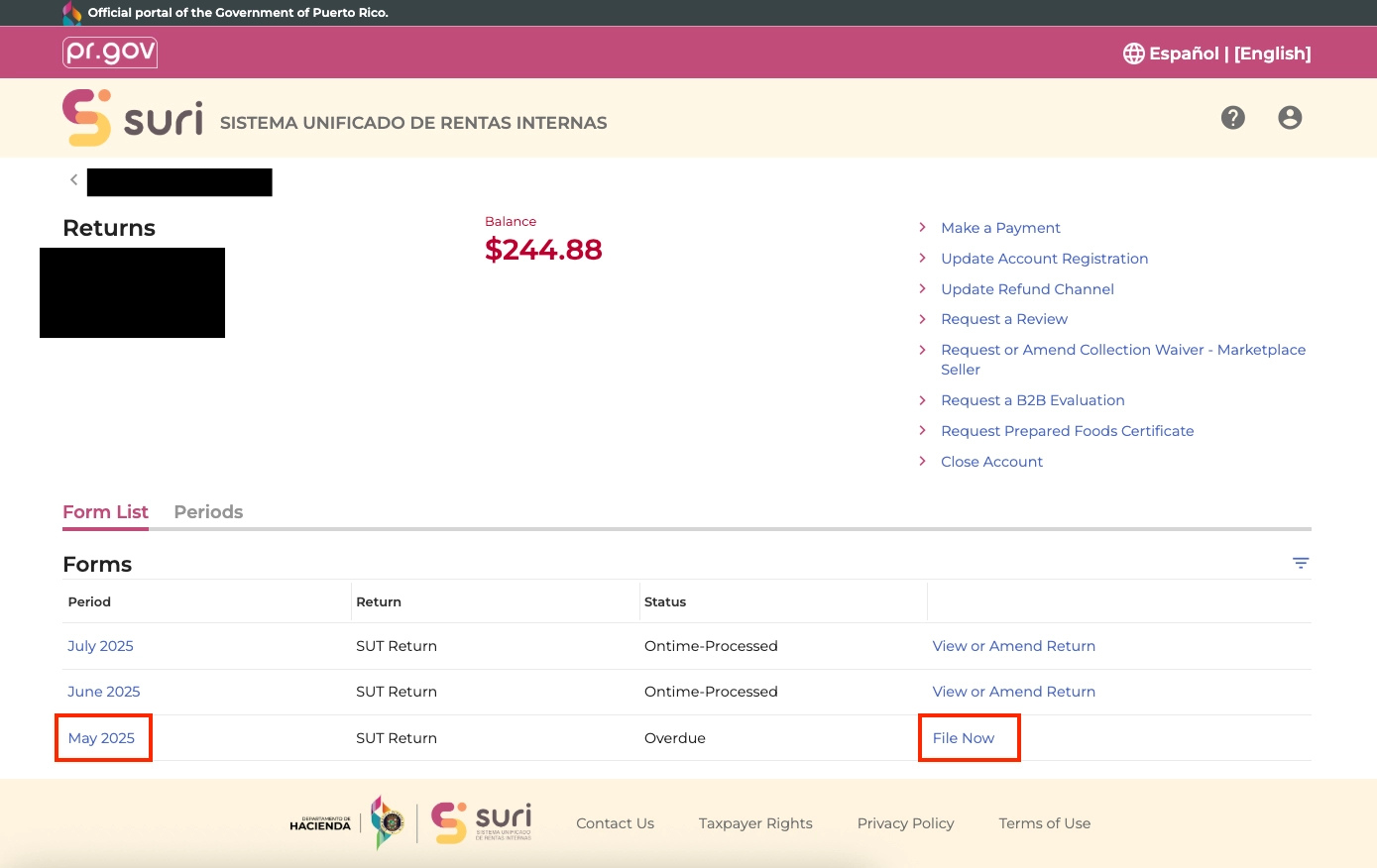

Next, navigate to the sales and use tax (IVU) return section, click on View Returns, Periods, and other options, and select the filing period for the month that you are filing.

To complete the remaining steps, you must confirm the amount of tax you are reporting. This will be done outside of the SURI system using whatever process you have in place to record taxable sales, tax collected, discounts, credits, penalties, or interest.

When you're ready with the correct amount due, click on the option to "File now" next to the month that you are submitting the tax returns for.

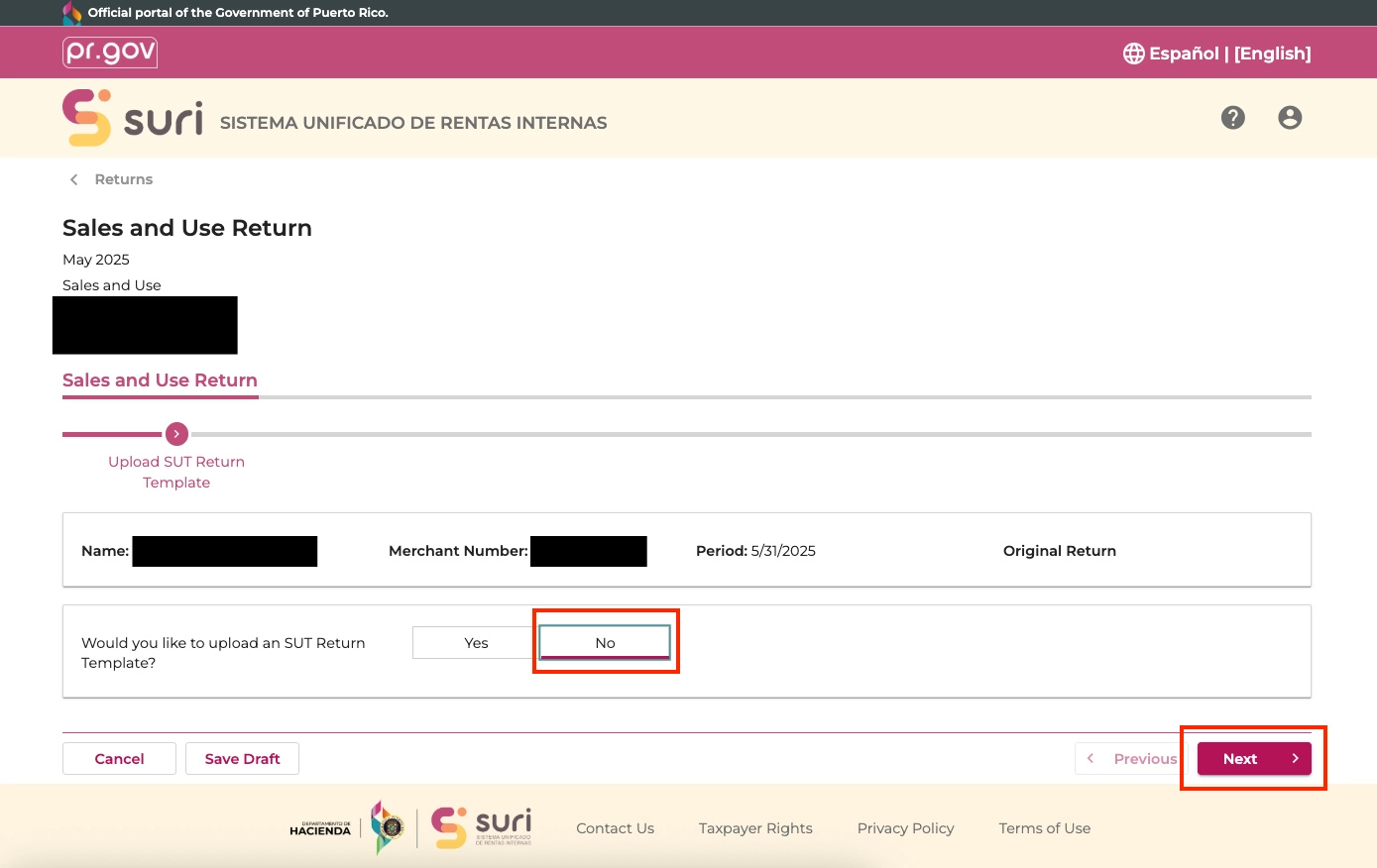

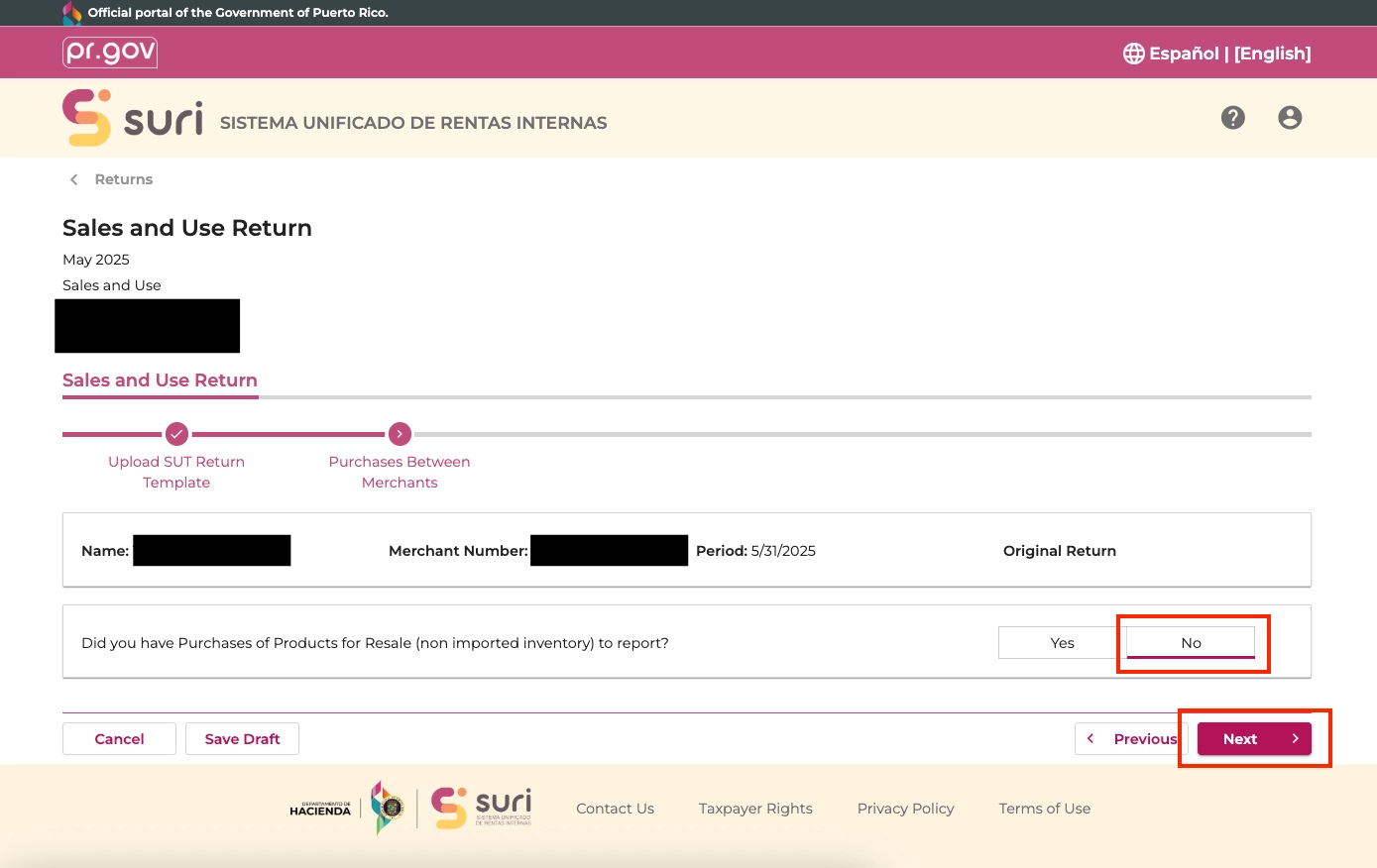

You will be asked if you want to upload a SUT return template, and you should select "No" if you're planning to complete the forms online rather than uploading a saved form.

You must next select whether you have Purchases of Products for Resale (non-imported inventory) to report. If you are not reporting purchases of products for resale, select "No."

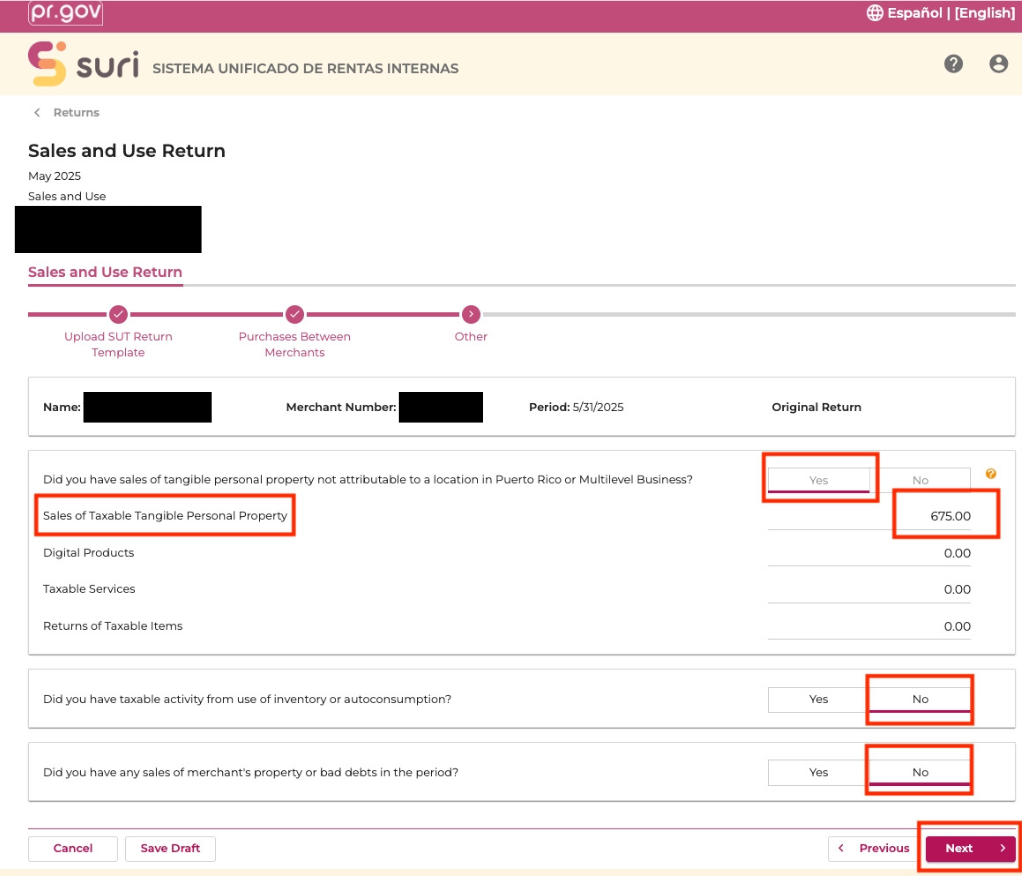

The next form will ask you if you have Sales of Tangible Personal Property. If you collected tax on products or services at the 11.50% rate, click "YES."

If your collected tax rate is below 11.50%, you will need to follow different steps for "Exempt rates or reduced rate products."

If you collected the standard tax on all products, enter the amount collected in the box that says "Sales of Taxable Tangible Personal Property." This amount will come from your accounting records, where you track tax collected.

If you collected tax on the sale of digital products or taxable services, record the tax collected in the appropriate box. You should also report any return of taxable income.

Finally, on this form, select whether you had taxable activity from the use of inventory or autoconsumption, or if you had early sales of merchant's property or bad debt.

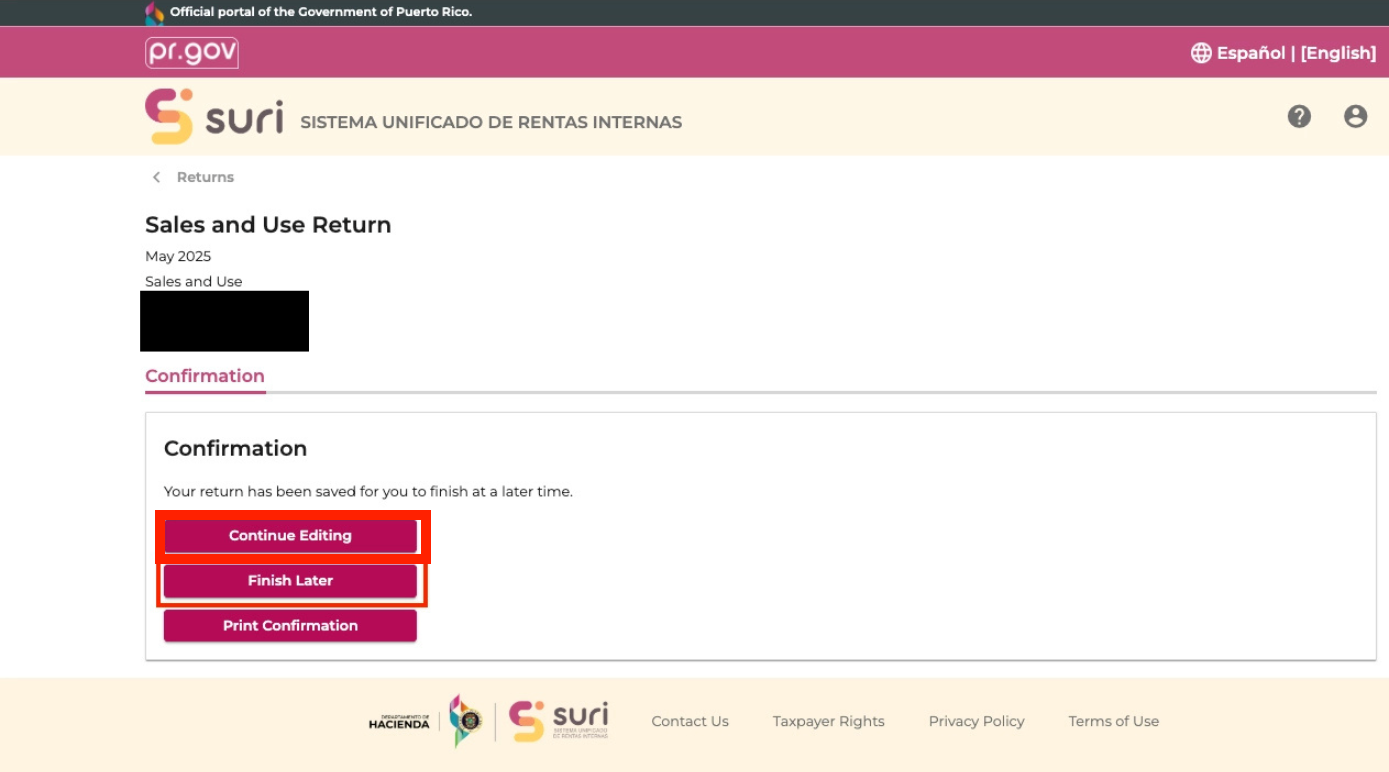

Once you have entered all of the correct tax amounts due, the last step is to review your forms and submit your final returns.

You can also save your progress as a draft if you need to return later.

Step 4: Remit payment (and claim the early filing discount)

You can make a payment electronically through SURI when you file your return. Use the online portal to pay the IVU due after any applicable credits are applied. Be sure to keep all records of your submitted form and payment receipts.

Tip: Puerto Rico may provide you with an early payment discount. Specifically, if you submit your returns and remit payment no later than the 15th of the month, you may receive a tax credit worth:

- 1.95% on the first $6,250 of IVU due

- 1% on any additional amount above that

If your IVU bill is $1,000 per month, that credit adds up to around $19.50. While that's not a fortune, it's a small amount of money without requiring any extra work on your part. It can also add up over time if you consistently pay early over many years of doing business.

What makes Puerto Rico's IVU different from U.S. state sales tax

Puerto Rico's IVU is different from state sales tax in the U.S. for multiple key reasons, most of which stem from the simple fact that Puerto Rico is a U.S. territory and not a U.S. state.

Because of this, Puerto Rico falls outside the standard Wayfair framework that informed the system of economic nexus rules, which apply across much of the U.S. It's also not part of the Streamlined Sales Tax (SST) effort that simplifies tax compliance in member states.

Puerto Rico also has a separate registration process, separate portal, and separate compliance requirements from any U.S. state, as you'll pay taxes to the Departamento de Hacienda de Puerto Rico and register, file and remit through SURI.

If you are registered in all 50 states, but sell within Puerto Rico, following the territory's tax rules is an additional compliance requirement. Its 11.5% combined rate is also higher than in many U.S. jurisdictions, so it's important to be aware of this obligation and the potential costs.

Who needs to file: Nexus in Puerto Rico

While Puerto Rico has its own tax compliance systems, it has some things in common with U.S. states. Specifically, you're only required to file and remit if you have either economic or physical nexus.

It's important to understand how nexus is established to understand your obligations. Here’s a look at each of them.

Physical presence nexus

Physical nexus refers to a physical presence in Puerto Rico. If you have physical nexus, you have an obligation to file and remit taxes. Your company doesn't have to be incorporated in or have a storefront to establish physical presence, either.

You may have physical nexus if you have any of the following in Puerto Rico:

- An office

- A store

- A warehouse

- Employees

Hiring remote workers or storing goods in Puerto Rico can trigger nexus, so be aware of these rules.

Economic nexus

Economic nexus refers to economic connections with the territory. In Puerto Rico, you have sufficient economic connections to establish nexus once you have either:

- $100,000 in gross sales to Puerto Rico customers in a calendar year, OR

- 200 separate transactions into Puerto Rico

You don't need to meet both requirements to establish economic nexus. You should track both the number of transactions and the transaction amount to make sure you're in full compliance.

And because Puerto Rico requires you to register 30 days in advance of the time you begin doing business locally, you must be proactive and begin the registration process early to avoid penalties.

Numeral offers free nexus tracking and can make this process easy.

Marketplace sellers

As mentioned above, marketplace facilitator laws task marketplaces like Amazon, eBay, and Etsy with the obligation to collect and remit sales taxes, including Puerto Rico's IVU.

However, you should verify both that the platform you're selling on is a marketplace facilitator (not all are, as it depends on the role it plays in the transaction) and that it covers Puerto Rico.

If you sell through your own website and a marketplace, you may still have independent obligations to register in Puerto Rico and to collect and remit sales taxes for transactions that occur off the marketplace, even if a marketplace facilitator handles taxes on some of your sales.

What's taxable in Puerto Rico

Puerto Rico imposes IVU on most tangible goods and many digital products at the 11.5% rate. However, there are certain exemptions to be aware of, as you do not have to collect or remit taxes on exempt sales.

You'll need to configure tax collection properly to collect tax only on non-exempt sales if you sell a mix of exempt and non-exempt goods. The table below shows some common items that are both taxable and exempt:

| Category | Exempt? |

|---|---|

| Unprepared food and groceries | Yes |

| Prescription drugs | Yes |

| Insulin | Yes |

| School uniforms | Yes |

| Items purchased for resale | Yes (with exemption certificate) |

| Raw materials for manufacturing | Yes (with exemption certificate) |

| Real estate transactions | Yes |

| Air and maritime tickets | Yes |

| SaaS / digital services | No—taxable at 11.5% |

| Prepared food and drinks | No—taxable |

What's generally taxable

The following goods are generally considered to be non-exempt taxable goods in Puerto Rico:

- Tangible personal property or physical goods shipped to customers in Puerto Rico

- Digital products, including downloaded software, digital files, and streaming services

- SaaS and cloud-based services. SaaS is taxed at the standard 11.5% rate, unlike in many (not all) U.S. states, where SaaS is exempt from sales or use tax.

- Prepared food and beverages

- Most consumer-facing services

Common exemptions

Some items are also generally exempt, including:

- Unprepared food and groceries

- Prescription drugs

- Insulin

- School uniforms

- Items purchased for resale (with an exemption certificate)

- Raw materials for manufacturing (with an exemption certificate)

- Real estate transactions

- Air and maritime tickets

Buyers claiming resale or manufacturing exemptions must provide the appropriate sales tax exemption certificate. Sellers should retain these to be audit-ready.

B2B services

Puerto Rico has a separate reduced-rate regime for certain designated professional services sold business-to-business.

This rate could be as low as 4%, but it can be complicated to determine when this rate applies.

Penalties for late filing and non-registration

If you fail to fulfill your IVU obligations in Puerto Rico, you can face fines and penalties. Some potential consequences include the following:

- Late or missing registration: Failure to register as required when doing business in Puerto Rico can result in penalties totaling up to $10,000. This is one of the steepest penalties that applies for failure to register

- Late filing: Puerto Rico charges interest and penalties on overdue returns and unpaid IVU balances. The late filing penalty is 10% of the liability reflected in the return

- Late payments: The late payment penalty ranges from 5% to 50% of the liability reflected in the return, with a 5% increase until the maximum penalty is reached. Repeat offenders face penalties totaling 5% to 100% of the liability reflected in the monthly return, with a 5% increase each month until the maximum penalty is reached.

- Failure to collect required IVU: If you establish a nexus but don't collect IVU, Hacienda can assess back taxes plus interest and penalties going back to when the obligation began.

If you realize you should have been filing and remitting taxes but weren't, Puerto Rico has a voluntary disclosure program through Hacienda. While this program can reduce or eliminate penalties, you should always consult with a tax professional before filing.

How Numeral handles Puerto Rico IVU

If you have IVU obligations in Puerto Rico, Numeral can take those obligations off your plate and ensure you fulfill all requirements. Numeral can automate the entire compliance process for you, including:

- Nexus monitoring: Numeral offers free nexus monitoring that tracks your sales in Puerto Rico and proactively alerts you when you're approaching or have crossed the $100,000/200-transaction threshold so you have time to take action.

- Registration: When nexus is triggered, Numeral handles the registration process through SURI on your behalf, including completing and submitting the Merchant's Registration Certificate application.

- Monthly filing and remittance: Numeral prepares and files your IVU return each month, remits your required payment to Hacienda, and ensures early-payment credits automatically.

- Expert review: While returns are taken care of automatically for you, we don't just auto-submit. Every return is reviewed by a tax expert at Numeral before submission.

- The Numeral Guarantee: If a filing is missed or we make errors that lead to an audit and penalties, we'll cover filing costs and any resulting fees.

- Pricing: Nexus monitoring is free with Numeral, while filing costs $75 and registration $150.

Numeral allows you to handle your sales tax obligations in Puerto Rico (as well as in every U.S. state and 80+ countries) in as little as five minutes a month.

[blog-post-inline-cta]

Puerto Rico sales tax (IVU) FAQs

Still need to know more? Here are the answers to some frequently asked questions about IVU in Puerto Rico.

Does Puerto Rico have sales tax?

Puerto Rico collects a tax called Impuesto sobre Ventas y Uso (IVU), which is the sales and use tax for the U.S. territory. The combined rate is 11.5%, charged on most goods and some services, including digital goods and SaaS.

Do I need to collect Puerto Rico sales tax if I sell online?

If you sell online, you may need to collect Puerto Rico sales tax. You will be obligated to collect the tax, called Impuesto sobre Ventas y Uso (IVU), when selling to customers in Puerto Rico if you establish physical or economic nexus.

Physical nexus involves having a physical presence in Puerto Rico, while economic nexus involves having 200 or more transactions or $100,000 or more in gross sales with customers in Puerto Rico.

How do I register to collect IVU in Puerto Rico?

To register to collect IVU in Puerto Rico, you must first register as a merchant through SURI. You'll need to provide your EIN, business name, and address, expected sales volume, and types of goods and services sold.

Once you've created an account, complete Form AS 2914.1 to register and request a Certificado de Registro de Comerciante. Be sure to register early, as you are required to obtain a certificate 30 days before you begin operations.

When is Puerto Rico sales tax due?

Puerto Rico requires you to file IVU returns and remit sales tax payments by the 20th of the month after the taxable sales occur. However, you become eligible for an early filing credit if you submit your returns and remit payment by the 15th.

Is SaaS taxable in Puerto Rico?

SaaS is taxable in Puerto Rico if you have economic or physical nexus. It's important that you collect tax at the correct rate and remit payments as required.

What's exempt from Puerto Rico's IVU?

Puerto Rico has several exemptions from its IVU, including unprepared food and groceries, insulin, prescription drugs, clothing items under $50, and both items purchased for resale or raw materials for manufacturing if you have the proper exemption certificate.